OMAHA, Neb. (May 1, 2025) — The Creighton University Mid-America Business Conditions Index, a leading economic indicator for the nine-state region stretching from Minnesota to Arkansas, moved above the 50.0 growth neutral threshold for a fourth straight month.

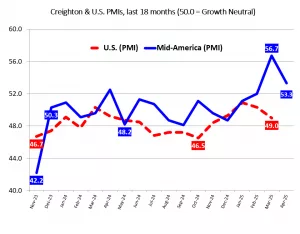

Overall Index: The Business Conditions Index, which uses the identical methodology as the national Institute for Supply Management (ISM) and ranges between 0 and 100 with 50.0 representing growth neutral, declined to a solid 53.3 from March’s stronger 56.7.

“The Creighton survey is recording significant volatility, much like other regional economic measures. Proposed and implemented tariffs are not only producing economic volatility but are damaging supply managers’ economic outlook and pushing input prices higher,” said Ernie Goss, PhD, Director of Creighton University’s Economic Forecasting Group and the Jack A. MacAllister Chair in Regional Economics in the Heider College of Business.

The Mid-America report is produced independently of the national ISM.

As indicated by a supply manager in the April survey, “The uncertainty (surrounding tariffs) is paralyzing.”

Employment: The April employment index tumbled to 44.9, its lowest level since November 2024, and down from 67.6 in March. “First quarter employment was pushed higher due to higher production in anticipation of the fallout from tariffs later in the year. April’s reading represented a return to manufacturing job losses in the region,” said Goss.

As reported by one supply manager in April, “Employees are concerned about the economy and their jobs.”

U.S. Bureau of Labor Statistics data show that the region shed 11,900 (-0.8%) manufacturing jobs over the past 12 months. The U.S. lost 74,000 (-0.6%) manufacturing jobs over the same time period.

Comments from supply managers in April:

- ‘While the tariffs seem painful, it is my opinion that this approach is the correct reset. The social economical great reset is theft and power.”

- “While the rest of the world seems to be focused solely on tariffs, Trump is playing 4d chess with China, who has fleckless disregard for the international community and the rule of law. They have been buying influence in the western hemisphere for years and thumbing their nose at the WTO and other world bodies who are helpless to stop them.”

- “If the U.S. doesn’t curb the Chinese ambitions, we will all be speaking Mandarin and Cantonese in the next decade! The unrest in the world today was created and is being perpetuated by China, Russia, Iran and other bad actors.”

- “The Chinese want to control Taiwan to keep U.S. influence out of the region with Japan and other smaller nations in their crosshairs. The U.S. is the only one capable of restoring global order with the support of its allies. The global economy will get worse before it gets better!”

- “The impact of the tariffs is just starting to be realized. Changes will be made now that the actual dollar impact is known.”

Wholesale Prices: The April price gauge rose to 65.0, its highest reading since May 2024, and up from 63.7 in March. “The regional inflation yardstick has clearly moved into a range indicating that inflationary pressures are moving higher. Even so, I expect the Fed to leave interest rates unchanged at its next meetings on May 6-7,” said Goss.

Approximately 65% of supply managers reported that rising tariffs and supply chain interruptions have resulted in higher input prices.

Roughly 85% reported impacts from tariffs, either via higher prices or supply chain interruptions.

As reported by an April survey participant, “Some companies will push through price increases. Some won’t be able to due to the elasticity (responsiveness) of demand.”

Confidence: Looking ahead six months, economic optimism, as captured by the April Business Confidence Index, sank to 35.3, its lowest reading since September 2024, and down from 37.5 in March. “Due to concerns regarding global economic tensions and rising tariffs, only one in four of supply managers expect improving business conditions over the next six months,” said Goss.

Inventories: The regional inventory index, reflecting levels of raw materials and supplies, expanded to 56.7 from March’s weak 32.5. “In order to front-run tariffs, firms have expanded inventories for three of the first four months of 2025,” said Goss.

Approximately 21.1% of supply managers reported that higher tariffs have pushed their firms to switch suppliers for a share of their inputs.

Trade: Recent uncertainty regarding tariffs and trade restrictions pushed trade numbers lower for April. New export orders slumped to 46.2 from 52.6 in March. As result of record imports for the first two months of 2025, supply managers pulled back on purchasing from abroad in March and April. The April import index fell to a record low of 12.5 from March’s 32.6.

According to U.S. International Trade Administration (ITA) data, the regional economy exported $14.7 billion in manufactured goods for the first two months of 2025, compared to $15.3 billion for the same period in 2024, for a 4.2% decline. In terms of export gainers, Oklahoma registered the top gain with a 11.4% addition, and South Dakota recorded the largest loss with a 24.5% reduction in the export of manufactured goods.

Other survey components of the April Business Conditions Index were: new orders declined to 52.9 from 55.9 in March; the production or sales index was unchanged at 55.4; and the speed of deliveries of raw materials and supplies increased to 56.8 from March’s 56.0. Higher readings indicate rising supply chain disruptions or delays.

The Creighton Economic Forecasting Group has conducted the monthly survey of supply managers in nine states since 1994 to produce leading economic indicators of the Mid-America economy. States included in the survey are Arkansas, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Oklahoma and South Dakota.

Below are the state reports:

Iowa: The state’s Business Conditions Index for April declined to 53.0 from 56.3 in March. Components of the overall April index were: new orders at 52.6; production or sales at 54.9; delivery lead time at 57.1; employment at 44.0; and inventories at 56.6. According to ITA data, the Iowa manufacturing sector exported $2.3 billion in goods for the first two months of 2025, compared to $2.6 billion for same period in 2024, for a 12.0% reduction.

Kansas: The Kansas Business Conditions Index for April sank to 51.1 from March’s 53.9. Components of the leading economic indicators from the monthly survey of supply managers for April were: new orders at 55.6; production or sales at 53.8; delivery lead time at 54.8; employment at 61.3; and inventories at 44.3. According to ITA data, the Kansas manufacturing sector exported $1.8 billion in goods for the first two months of 2025, compared to $2.0 billion for the same period in 2024, for a 9.2% reduction.

Missouri: The state’s April Business Conditions Index fell to 48.1 from March’s 51.5. Components of the overall index from the survey of supply managers for April were: new orders at 51.9; production or sales at 52.6; delivery lead time at 53.8; inventories at 47.7; and employment at 34.3. According to ITA data, the Missouri manufacturing sector exported $2.6 billion in goods for the first two months of 2025, compared to $2.4 billion in goods for the same period in 2024, for a 7.6% gain.

Nebraska: For the 10th time in the past 11 months, Nebraska’s overall index climbed above the growth neutral threshold. The state’s April Business Conditions Index stood at 50.1, down from 53.8 in March. Components of the index from the monthly survey of supply managers for April were: new orders at 52.2; production or sales at 53.5; delivery lead time at 55.1; inventories at 51.3; and employment at 38.2. According to ITA data, the Nebraska manufacturing sector exported $1.0 billion in goods for the first two months of 2025, compared to $1.1 billion for the same period in 2024, for a 6.5% reduction.

South Dakota: The April Business Conditions Index for South Dakota decreased to 55.8 from March’s 61.6. Components of the overall April index were: new orders at 53.0; production or sales at 56.1; delivery lead time at 59.0; inventories at 61.4; and employment at 49.3. According to ITA data, the South Dakota manufacturing sector exported $250.9 million for the first two months of 2025, compared to $332.1 million for the same period in 2024, for a 24.5% reduction.